Table of Content

To get preapproved, you’ll need to provide your lender with documents they’ll use to verify your personal, employment and financial information. Just like other loans or credit cards, mortgage prequalification doesnt hurt your scores since its also based on a soft inquiry. Having your credit report evaluated is a mandatory and necessary part of the mortgage process, Bey said. Because of that fact alone, there would be no benefit to the bank or anybody involved in the transaction to punish the prospective buyer for having their credit evaluated by a bank. When you apply for a loan, lenders make hard inquiries into your credit file to learn if you are a good credit risk.

Each lender’s process is different, but they’ll generally review your credit history, income, assets and debts before deciding to grant a preapproval and, if so, for what amount. First, it gives you an idea of how much you can borrow, which will help narrow down your search to houses in your price range. But remember that just because you’ve been preapproved for an amount doesn’t mean you have to borrow the maximum. That’s because many mortgage lenders use your gross monthly income as a factor in determining how much you qualify for. Many are forgiving when it comes to borrowers who are rate shoppingthey don’t treat all inquiries the same.

Can A Pre-Approval Affect My Credit Score?

But getting pre-approved is absolutely essential to confirm that you can afford to buy the kind of house you want and to strengthen your offer when you find the right home. When you’re ready to make an offer, you’ll have a pre-approval letter to confirm that you can qualify for a home loan. This makes your offer more appealing to sellers because they get extra assurance that you’ll be able to secure the financing to complete the purchase.

Because the process involves submitting a mortgage loan application, there’s no way to avoid the hard credit inquiry triggered by the mortgage pre-approval process. To determine whether or not you qualify for a mortgage, an underwriter must evaluate your credit and look at your earnings, debt and savings. Seeking mortgage preapproval before shopping for a home can save time and give you an edge over rival buyers who haven't done so.

How to choose the best mortgage lender

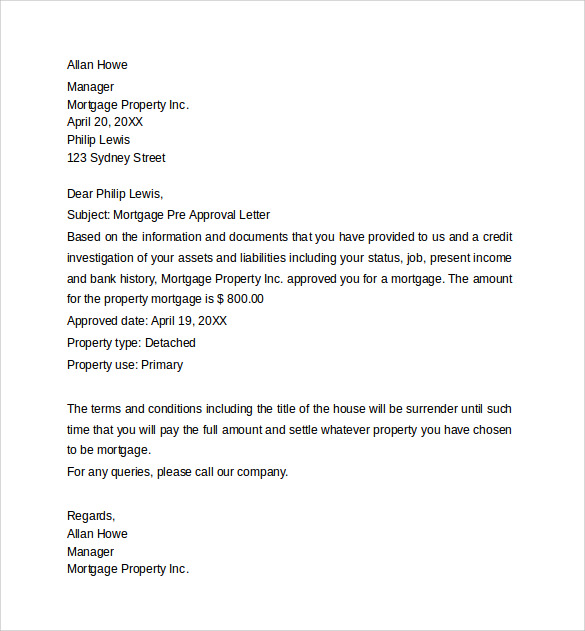

You will be asked to provide information on your liabilities, assets, valid ID, and employment. Your application will be reviewed and results are typically released to you in one to two days. You are under no obligation by getting pre-approved, but you want to be comfortable with the amount and terms of your pre-approved mortgage. That’s why it’s essential that you review all your personal expenses and have a good idea of your future expenses before you talk with a mortgage broker or lender about pre-approval. When you get a mortgage approval, your lender estimates how much you can afford to borrow, what your interest rate could be and how much your mortgage payments could be. You and your real estate agent can use this information to focus on homes you can afford.

They might also ask you to provide copies of bank statements to show how much money you have available and what you’ve saved for a down payment. The pre-approval typically requires a hard credit inquiry, which decreases a buyer’s credit score by five points or less. A mortgage pre-approval is a detailed review of your finances conducted by a lending institution. Typically, you will provide information about your income, outstanding debt, credit history, and ability to make a down payment. If you later decide to submit an application and agree to a hard credit pull, your credit score may be impacted. You will receive nothing but a hard inquiry on your credit history, a drop in credit score, and people trying to contact you about your new loan .

Get quotes from different mortgage lenders

A credit score of 750 or higher is considered excellent and better for lending to secure lower interest rates. Seeking pre-approval six months to one year in advance of a serious home search puts you in a stronger position to improve your overall credit profile. Youll also have more time to save money for a down payment and closing costs. A mortgage approval also proves to sellers that you can afford the home theyre selling. Without first securing approval from a lender, the seller might not trust your offer is genuine. Your offer might not be accepted and even if it is, offering to buy a home without lender approval can slow down your mortgage loan application.

NerdWallets debt-to-income ratio calculator can help you estimate your DTI based on current debts and a prospective mortgage. Lenders prefer borrowers with a DTI of 36% or below, including the mortgage, though it can be higher in some cases. During the preapproval process, you’ll send copies of your most important financial documents so that your lender can verify your income. These are typically documents like your last 2 months of bank account statements, two most recent paycheck stubs, your last two tax returns and your W-2 forms from the last 2 years.

If you’re like a lot of people, your next thought might be to wonder what this will do to your credit score. After all, the last thing you want is a ding to your credit when you need it in the best possible shape. The Canada Mortgage and Housing Corporation recommend that at least one applicant in a mortgage has a minimum credit score of 680 if you are making a down payment of less than 20%. Having a higher credit score means you may have some flexibility on the amount of down payment you will need to provide upfront to secure your home loan.

This will help you to decide on the best lender without affecting your credit score. A mortgage broker is also helpful when it comes to finding the right lender. They can assess your situation and give you an idea of your borrowing capacity with lenders without making formal enquiries. In short, yes, getting pre-approved for a mortgage can affect your credit score. But the impact is likely to be less than you expect and shouldn’t stand in the way of you getting final approval for a mortgage.

As you get closer to buying a home, there are a few steps you can take to help ensure you get a mortgage thats right for you, and ultimately, the home you want. Just remember, getting your credit checked is part of the process, and understanding what it encompasses will help as you pursue homeownership. Heres what you need to know about getting prequalified and preapproved for a mortgage and how a credit check can potentially affect your credit score. Mortgage preapproval is a lenders conditional approval for a home loan in the form of a preapproval letter. Keep in mind that preapproval is not a guarantee that youll be approved for the mortgage, and the terms youre offered may change after you submit a complete, formal mortgage application. You may want to monitor your other two credit reports as well, because mortgage lenders may use all three of your reports and credit scores based on each report.

Founded in 1976, Bankrate has a long track record of helping people make smart financial choices. Weve maintained this reputation for over four decades by demystifying the financial decision-making process and giving people confidence in which actions to take next. So a pre-approval could actually save you time and money, despite being a task that needs to be taken care of upfront. But nowadays, with so few properties on the market, and so many multiple-bid situations, its often a requirement just to hear back from the sellers agent.

Being able to set an accurate budget is another advantage of getting pre-approved. When you know the mortgage amount you are qualified to obtain from a lender, you can make more accurate decisions on which homes you want to afford and see in person. Knowing your mortgage amount, down payment, and monthly payments up-front is an integral part of the house-hunting process. However, the impact on a home buyer’s credit score declines as time passes, and the hard inquiry becomes less relevant. Hard inquiries into your credit for the purpose of issuing a pre-approval may temporarily have a small impact on your credit score.

It’s important to do your homework before choosing potential lenders. A mortgage prequalification is an estimate of what you may be able to borrow on a mortgage using basic financial information. Prequalifications are considered to be less reliable than a mortgage pre-approval because the information is typically not verified. It sounds great in theory but the problem is that not all lenders are providing this information to credit reporting agencies. Where it can be a problem is if you’ve applied for a pre-approval with multiple lenders in a short timeframe. In some cases, it may even improve your credit score, particularly if you’ve never had any enquiries on your credit file before.

In some cases, errors in your credit report can be a sign of identity theft or fraud. With that information in hand, you know where you can set your budget. Guild Mortgage Company 5887 Copley Drive, Floors 1, 3, 4, 5, 6, San Diego, CA 92111; For more licensing information, please visit /licensing.

We challenge inaccurate negative items with the bureaus and your creditors. We place links on our website to our affiliates, and when you click those links, our affiliates compensate us for it. Our relationships with our affiliates may affect which products we feature on our site and where these products appear in our articles.

No comments:

Post a Comment